Call Today! 888-234-8376

What is Universal Life Insurance?

February 25, 2020

Like whole life, universal life is designed to cover you for your entire life while growing your cash value. But universal life is typically much cheaper than whole life.

Universal life is also a lot more flexible. Even after you buy a policy, you may be able to adjust your length of coverage, death benefit amount, and premiums. Depending on what kind of universal life policy you buy, you may even decide how to invest your cash value.

This type of life insurance isn’t right for everyone, however. It’s much more complicated than both term life and whole life. You may also risk losing your life insurance coverage with this policy if your cash value investments don’t pan out or you fail to fund the policy adequately.

Here’s what you should know about universal life insurance before you decide if this complex but versatile policy is right for you.

How universal life insurance works

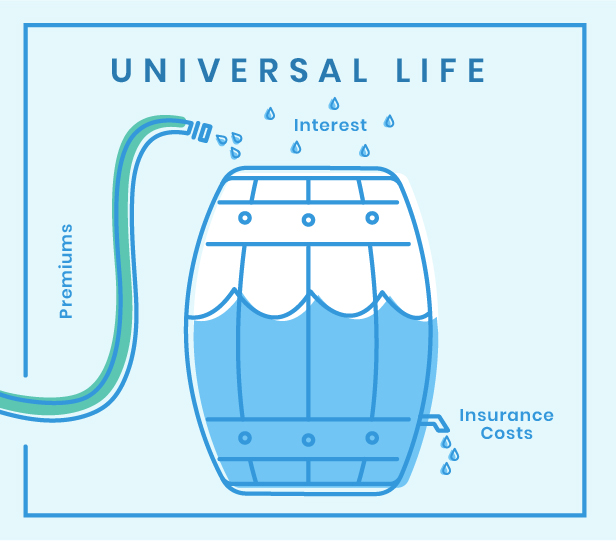

Think of your universal life insurance policy like a barrel, but instead of holding water, this barrel holds money. You add money to your policy by paying your premiums, like filling a barrel with a hose. Ideally, your policy should also grow naturally by earning interest, like a barrel filling up with rainwater.

Call today: 888-234-8376

Money comes out of your policy to pay for your life insurance coverage, like a gardener tapping the barrel to water a bed of flowers. If there isn’t enough money in your policy, however, paying insurance costs could drain your policy—and put your coverage in jeopardy.

Let’s look at the four parts of your universal life insurance barrel: your premiums, cash value, death benefit, and insurance costs. Understanding how they all work can help you avoid risking your coverage.

Universal life insurance premiums

With universal life insurance, you can choose how much you pay in premiums—to some extent, that is. Your premiums must be enough to cover the cost of insurance, or your policy will lapse. But if your barrel is topped off, you may be able to reduce (or skip) a premium payment once in a while.

Premiums can also determine how long your coverage lasts. While premiums are flexible, most insurers include a minimum premium and a target date premium in your policy. If you pay the minimum premium, the insurer guarantees you’ll keep your coverage for the current year.

The target date premium is higher than the minimum and designed to ensure coverage for a specific number of years. When you see policies advertised as “Universal until age 85” or “UL121,” these policies have target date premiums that ensure coverage until you turn 85 or 121, respectively. Of course, if you pay even higher premiums, you could keep your coverage indefinitely.

A word of caution

If you choose a type of universal life insurance policy that ties your cash value growth to the stock market, paying the target date premium may not guarantee you’ll keep your coverage until your target date. If the stock market drops—and your cash value along with it—you may need to pay higher premiums to keep up with the cost of insurance.

Universal life insurance cash value

The unique part of universal life insurance is how the cash value works. When you pay your premiums, some of these funds go toward building your cash value, just like whole life insurance.

But with universal life insurance, you have more options in how you grow your cash value. Depending on the type of universal life policy you buy, your cash value accumulation could be tied to a stock market index such as the S&P 500. Or, you could choose a policy that allows you to invest your cash value directly in the stock market.

If growing your cash value is like collecting rain in your life insurance barrel, then choosing a type of universal life insurance policy is like designing a collection system with strategically-placed rain gutters and spouts. If your strategy is solid, you could fill your barrel quickly—provided it rains enough.

Some universal life insurance policies come with guaranteed interest rates for your cash value, essentially ensuring a specific amount of rain. But other policies have no guarantees, and a downturn in the economy could result in a drought.

Either way, you’ll likely need to continue topping off the barrel yourself by paying regular premiums, but if your cash value does well, you may be able to skip a premium here and there. If your cash value grows slowly, you may need to pay extra premiums to keep your policy funded.

Universal life insurance death benefit

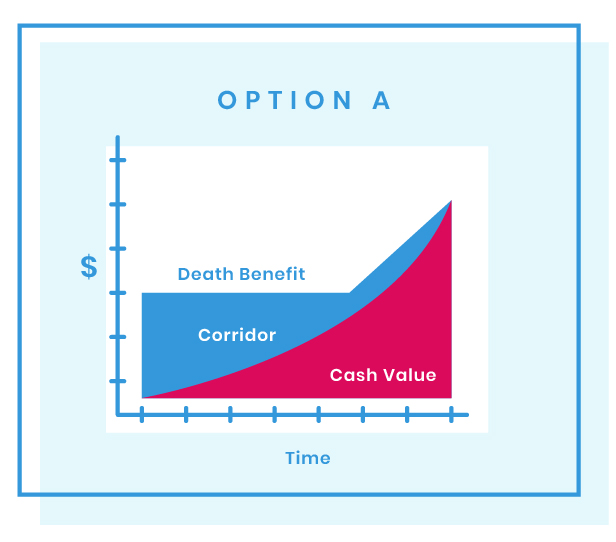

When you buy your universal life insurance policy, you can choose from two types of death benefits. A level death benefit is called Option A, and an increasing death benefit is called Option B.

Universal life insurance with Option A

With Option A, you’ll have a (mostly) level death benefit. Let’s say you buy a $100,000 universal life insurance policy with Option A. The moment you have coverage, your death benefit will be $100,000 and will stay the same through most of the life of your policy.

If your cash value grows enough, it may eventually approach your death benefit. When it gets close to $100,000, the insurer will begin raising your death benefit to ensure your cash value never exceeds your death benefit. As your cash value grows, the insurer will maintain this gap by continuously increasing your death benefit.

The difference between your death benefit and accumulated cash value is called the Universal Life Corridor. You may also see it labeled “pure insurance.” And as you can see from the above graph, the corridor shrinks over the life of your policy.

Universal life insurance with Option B

If you choose a universal life insurance policy with Option B, your corridor will stay the same throughout the life of the policy. Essentially, your death benefit will grow by the same amount your cash value accumulates. Of course, if you set up your cash value to fluctuate with the market, your death benefit may shrink in a downturn, unless you keep your barrel stocked with enough premiums.

Death benefit payout vs. policy maturity

Whether you have a level death benefit or an increasing death benefit, your policy must be in force when you pass away in order for your beneficiaries to receive a payout. The payout will match your death benefit at the time of death, and it will be partially covered by your cash value. Your beneficiaries won’t receive a separate cash value in addition to the death benefit.

But let’s say you choose universal life to age 85, and you reach your 85th birthday. Will your coverage end like term life insurance? Not exactly. At this time, your policy matures. Your coverage will end, but you’ll receive your cash value as a payout.

Universal life insurance costs

The insurance portion of your universal life policy comes in the form of annual renewable term (ART) with guaranteed renewability. With annual renewable term, your coverage costs go up each year. Each year’s increased rate is what it costs the insurer to maintain your policy at your current age and death benefit.

ART acts a bit differently in a universal policy, however. Your rate isn’t based on your death benefit, but the difference between your death benefit and your cash value (the Universal Life Insurance Corridor, mentioned above). If you choose a $500,000 death benefit and your cash value sits at $100,000, for example, your insurance costs will be based on insuring you for the difference ($400,000).

The idea is, as your cash value grows, it should outweigh the additional cost of insuring you as you age. But as we’ve seen, how your cash value grows depends on the type of universal life policy you choose. So, without further ado, let’s look at those options.

Types of universal life insurance

Universal life insurance works a little differently depending on the type of policy you choose. In addition to just plain ole’ straight universal, the possibilities include indexed, variable, guaranteed, and group universal life.

Indexed universal life insurance

Indexed universal is named after how the cash value works. Instead of your policy growing at a consistent rate, your interest rate is tied to an established stock market index, such as the S&P 500. Keep in mind, you won’t be investing directly in the stock market, and your interest rate will likely sit a little lower than the actual index it follows.

Learn more about indexed universal life insurance.

Variable universal life insurance

Variable life insurance allows you to use your cash value to invest directly in the stock market. You’ll have access to higher interest rates if your investments perform well, but you’ll also risk negative interest rates in a downturn.

If you’re interested in a variable life insurance policy, talk to an agent who is licensed to sell these products.

Guaranteed universal life insurance

Unlike other types of universal life insurance, guaranteed universal removes the risk of losing your coverage if your cash value runs out. Guaranteed universal is typically the cheapest form of permanent life insurance, but don’t expect your cash value to multiply quickly.

Learn more about guaranteed universal life insurance.

Group universal life insurance

Most group life insurance is term life, but some employers offer permanent life insurance options. Although rare, group universal life insurance can be cheaper than individual universal life insurance policies.

Pros and cons of universal life insurance

Advantages

Advantages Flexibility

Flexibility- Permanent coverage

- Cash value

- Low cost

Disadvantages

Disadvantages Complexity

Complexity- Risk

- Not the cheapest

- Increasing insurance costs

Advantages of universal life insurance

Flexibility

Universal life insurance is some of the most flexible coverage you can buy. Depending on which policy you choose, you can vary your premiums, death benefit, coverage length, and cash value growth.

Permanent coverage

Universal life insurance won’t end after a specific number of years. If you fund your policy sufficiently, it could last your entire life.

Cash value

Universal life insurance includes a cash value designed to grow over time. You can use this cash value to take out policy loans, and if you cancel your coverage, you may receive some of your cash value. Some of the things you can do with your cash value come with tax implications, though, so learn more about how life insurance is taxed.

Low cost

Universal life insurance offers many of the advantages of whole life insurance, but it’s typically cheaper. In fact, guaranteed universal life may be nearly as cheap as term life for some applicants.

Disadvantages of universal life insurance

Complexity

Depending on the policy you buy, universal life insurance can become pretty complicated. Make sure you read your policy completely and consider having a lawyer or financial advisor look it over as well.

Risk

Unless you buy guaranteed universal life insurance, your cash value—and therefore your coverage—could be at risk if you don’t properly fund your policy or if your cash value doesn’t earn enough interest.

Not the cheapest

While universal life is less expensive than whole life, it’s still more expensive than term. If you don’t need permanent coverage, you could save money by choosing term life instead.

Increasing insurance costs

The coverage portion of your universal life insurance policy acts like annual renewable term, so your actual coverage rate will increase each year as you age. While your cash value growth is designed to offset these costs, there’s no guarantee. As a result, insurers typically have you overfund the policy when you’re younger to ensure your costs remain manageable later in life.

Universal life insurance company reviews

Universal life insurance has a ton of advantages over term and whole life. It’s more flexible and offers permanent coverage at a middle-of-the-road price. But it’s also complex and could be risky, so it’s not right for everyone.

If universal life insurance seems like the right fit for you, your next step is choosing the right life insurance company. Luckily, we’ve sifted through tons of insurers to find out which ones stand out for their universal life insurance products. So check out the best universal life insurance companies. Happy hunting!

Not sure universal life insurance is for you? Check out these other topics:

- Learn about all types of life insurance

- Learn about the differences between universal life and whole life insurance.

- Check out term life insurance instead.

- If you’re looking to cover only end-of-life expenses, read about final expense life insurance.